Standardizing Financial Reports Across Multiple Communities

Written by: Stephen Smellie

Published on: May 22, 2026

If you’re a community association manager with a portfolio, you’re not just one board’s point of contact, but you’re every board’s point of contact. You’re tracking assessments, monitoring reserves, coordinating vendors, navigating state-specific compliance requirements, and doing all of it simultaneously across communities that each have their own governing documents, their own financial histories, and their own expectations of you. The challenge isn’t really the volume, though. You can manage volume. The real challenge is variation.

Each community you serve operates under its own CC&Rs, bylaws, and applicable state law, and those documents often dictate how and when financial reports must be prepared, reviewed, and distributed. Reserve contribution requirements, special assessment thresholds, and meeting notice timelines are rarely identical across communities. So when you’re managing eight communities at once, you’re effectively operating under eight different financial rulebooks.

Without a standardized reporting framework to sit underneath all of that variation, your system breaks. At the portfolio level, that risk is multiplied by every community you add to your workload. At the same time, 73% of homeowners now expect real-time access to their association’s financial data – and poor accounting practices have been linked to board liability, regulatory fines, and special assessments averaging $2,000 to $5,000 per household.

That tells you the bar for financial transparency and good accounting practices has moved. Standardizing financial reports across multiple communities is how you meet that expectation. And to achieve that, let’s start with the foundation: the core financial reports every community in your portfolio should be maintaining.

The core financial reports that every community in your portfolio must maintain

Before you can standardize anything, you need to agree on what the standard package actually includes. Across the industry, six reports form the financial core that every association, regardless of size, age, or complexity, is expected to maintain.

- Balance sheet: It shows what the association owns (assets), what it owes (liabilities), and the resulting equity. If a community’s financial position is deteriorating, the balance sheet is usually the first place it shows up.

- Income statement: It tracks assessment income and other revenue against actual operating expenses and tells you whether the association ended the period with a surplus or a deficit. For boards, it answers the question they ask every month: Are we on budget?

- Cash flow statement: This statement tells you what was earned and spent. The cash flow statement tells you what actually moved. A community can look profitable on paper and still not have the liquidity to cover next month’s vendor payments. The cash flow statement breaks down inflows and outflows across operations, investments, and financing. And because it excludes non-cash items, it gives you the clearest picture of whether a community can actually meet its near-term financial obligations.

- General ledger: It’s the complete transaction-by-transaction record of everything that has moved through the association’s accounts, categorized by income, expense, asset, and liability. When something looks off on the income statement, the ledger tells you exactly what happened: which vendor, which invoice, which account it was coded to. Without it, none of your other reports can be fully trusted.

- Cash disbursement ledger: Where the cash flow statement gives you the big picture of money going out, the cash disbursement ledger gets specific. It records every payment the association makes – date, amount, payee, and purpose, covering both cash and check transactions. This report is what makes unauthorized or miscoded spending visible.

- Reserve fund statement: The reserve fund statement tracks how well-funded the association’s reserves are relative to its long-term capital needs. It’s the statement that tells whether the community is building toward a financial crisis and heavy special assessments.

Choosing and enforcing a uniform accounting method

Associations can choose from three recognized methods: cash basis, accrual basis, and modified accrual. Each one tells a different version of the same financial story. When you standardize the accounting method across your portfolio, that means you can exactly know the financial story of a community because you already know what the method shows and what it leaves out. But before you choose the method to use across your portfolio, let’s see what each method shows and leaves out.

Cash basis accounting

Cash basis is exactly what it sounds like: you record revenue when money is received and expenses when they’re paid. It works like a personal checking account – straightforward, easy to follow, and surprisingly limited for anything beyond the simplest financial picture.

Under the cash basis, accounts like Assessments Receivable, Prepaid Assessments, and Accounts Payable don’t appear on the balance sheet at all. Unpaid assessments and outstanding invoices are essentially invisible until cash actually moves. That means your financial statements can look healthier or shakier than they actually are. For you, overseeing a portfolio of eight or more communities, a cash basis creates a system-wide blind spot where the most important financial signals are hidden.

Accrual basis accounting

Accrual accounting works on a fundamentally different principle: transactions are recorded when they’re earned or incurred, regardless of when cash actually changes hands. Revenue shows up when it’s owed, not just when it’s collected. Expenses are recognized when they’re incurred, not just when the check clears. The result is a complete financial picture, one that includes what the association is owed, what it owes, and where things actually stand at any point in time.

Accrual is also the only method that conforms with GAAP, and it’s the standard used by virtually every professional HOA accounting firm for final reporting. If any community in your portfolio works with a CPA, has plans to borrow money, or is subject to state financial reporting requirements, accrual basis is the expectation. And because we’re talking about standardizing reporting across multiple communities, it means if one community needs accrual basis accounting, then that becomes your new standard.

Modified accrual basis

Modified accrual splits the difference. Revenue is recorded when earned (like accrual), but expenses are recorded when paid (like cash basis). It’s more informative than a pure cash basis and less complex to maintain than full accrual, which makes it appealing for internal, month-to-month reporting.

But it comes with a significant limitation: modified accrual is not GAAP-compliant. That means it can create extra work at audit time, complicate year-end reporting, and fall short of any state requirements that mandate GAAP-based financials. For portfolio CAMs, this is the ceiling of modified accruals’ usefulness – it can work for internal interim reporting, but it cannot anchor your year-end statements, audited financials, or any reporting that goes outside your office.

Why accrual is the right standard for a portfolio

When you’re managing a single community, the gaps in cash or modified accrual accounting are workable. You can mentally track outstanding invoices and delinquent accounts. But when you’re running ten or twelve communities through a single reporting cycle, those gaps compound into something much harder to manage.

Accrual accounting is the only method that makes your reports directly comparable across communities because every balance sheet is showing the same complete financial reality: what’s been collected, what’s outstanding, what’s owed, and what’s been paid.

Another thing, I said that if any community in your portfolio works with a CPA, has plans to borrow money, or is subject to state financial reporting requirements, the accrual basis is the expectation. And because we’re talking about standardizing reporting across multiple communities, it means if one community needs accrual basis accounting, then that becomes your new standard.

Understand state laws governing accounting methods

In some states, the accounting method to use isn’t even a choice left to the board or management company. It’s legislated. California is one of the most prescriptive examples: Civil Code Section 5300(b)(1) requires that annual operating budgets distributed to members follow the accrual basis. And under Civil Code Section 5200(a)(3)(d), when a homeowner formally requests financial records, those records must meet accrual or modified accrual standards.

So, the practical takeaway for anyone managing associations across multiple states is straightforward: standardize on accrual accounting across your entire portfolio. It eliminates the need to track which method applies to which community, keeps you compliant in the jurisdictions with the strictest requirements, and gives you the consistent, comparable financial data you need to actually oversee your portfolio.

Standardizing reserve fund reporting across your portfolio

Every community in your portfolio has a reserve fund. But here’s the harder truth: not every community is managing, tracking, or reporting it the same way. And without proper reporting, a community can look perfectly healthy on its monthly income statement while accumulating a crisis in its reserve account. So, standardizing how reserve funds are defined, studied, segregated, and reported across every association you manage is the baseline you should already be operating from.

Start with a reserve study

You can’t properly report on a reserve fund without a reserve study anchoring it. A reserve study is a comprehensive financial and physical analysis of the community. It inventories every common area component, evaluates its current condition and estimated remaining useful life, and then builds a 30-year funding plan based on what it will cost to repair or replace those components over time.

For a portfolio manager, the reserve study is what transforms the reserve fund from a single balance line on a report into something meaningful and actionable. It is what tells you whether the current funding level is appropriate, what the annual contribution should be, and how far off track a community might be. Normally, reserve funding represents 15% to 40% of an association’s total budget, making it one of the most significant line items in any financial plan.

Industry best practice calls for a full reserve study with a site visit every three to five years, with annual financial updates in between. And here’s something worth noting: Association Reserves’ 2026 Industry Insights Report found that more frequent reserve study updates are directly associated with lower rates of new special assessments. So, as you start standardizing, I recommend you get a fresh study or at least a recent one as your foundation.

Keep operating and reserve funds separate

Reserve fund standardization doesn’t stop at reporting. It requires that reserve funds be physically and legally separated from operating funds, in the association’s bank accounts and in its accounting records. In fact, it’s a legal requirement in many states.

For example, California Civil Code § 5510 explicitly prohibits HOAs from using reserve funds for operating expenses except under very strict guidelines. Florida Statute 718.111 requires boards to manage reserve funds as a fiduciary responsibility. And beyond the legal exposure, there’s a tax risk. If reserve money isn’t held in a separate account, the IRS can treat it as taxable income to the association.

How to report reserve health

The universal benchmark for reserve fund health is the percent funded figure, the ratio of the association’s current reserve balance to the theoretically ideal fully funded balance as calculated by the reserve study. Here’s how the industry reads that number:

- 75% or higher: Very good to excellent

- 70%–74%: Good to very good

- 65%–69%: Acceptable

- Below 50%: Escalating risk; treat as urgent

- Below 30%: Critically underfunded; high risk of special assessments

But here’s the nuance: percent funded should never appear in isolation on a board report. A community can show a healthy percent funded figure while still facing cash flow shortfalls in specific years. Always cross-reference that number against projected balances and planned expenditures before presenting it to the board.

Apply this standard uniformly across every community you manage. Report the reserve fund balance and percent funded at least annually, target 70% funded or higher as the long-term goal, and use the reserve study to define the contribution path to get there.

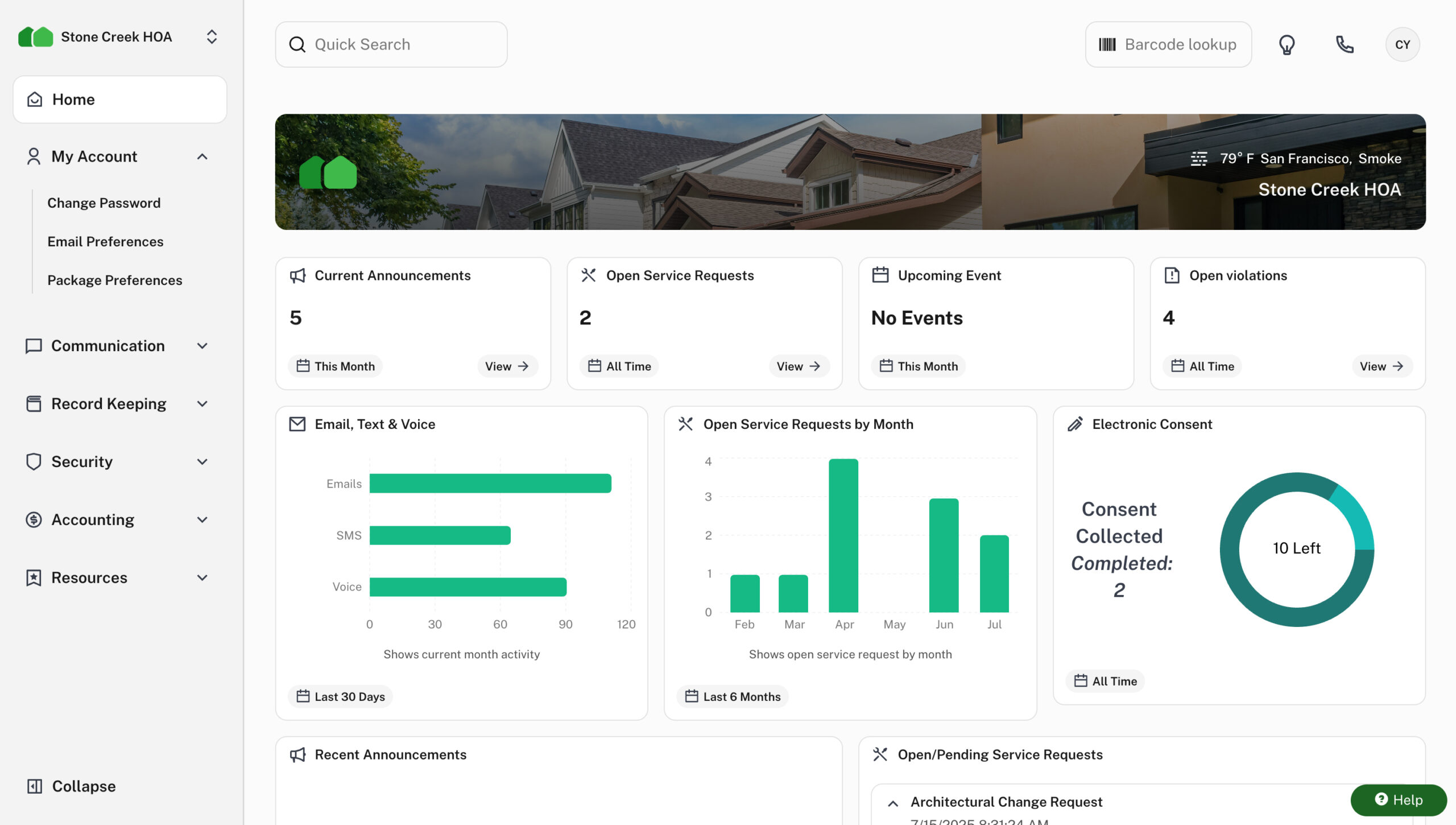

Using technology to simplify standardization

Getting your financial reporting framework right – the right reports, the right accounting method, consistent reserve tracking – is the strategic work. But if you’re managing eight, twelve, or twenty communities and you’re still relying on manual processes to hold all of it together, you’re going to hit a ceiling. The right technology platform is what turns a well-designed reporting structure into something you can actually sustain at scale without burning out your team or letting things slip through the cracks.

What to look for in a multi-community financial management platform

If you’re overseeing multiple associations, you need a platform that supports bulk actions, master dashboards, and cross-portfolio reporting. These tools reduce duplicated effort and give you visibility across all your communities without requiring you to open a dozen separate reports just to get oriented.

Beyond that, the platform should handle the full accounting lifecycle: budgeting, reserve fund tracking, audit preparation, and custom reporting that’s compliant with state and IRS requirements. It should also integrate with the other tools your company depends on, so data isn’t living in silos.

What matters most at the portfolio level is centralization paired with community-level flexibility. You need consistent standards enforced across every association, while still respecting that each community has its own governing documents, fiscal year, and board preferences. That means the platform needs centralized controls with configurable settings at the community level.

How automation improves standardization as you scale

Automation removes the human entry step from the equation. With direct bank integration, transaction data flows from the bank into your accounting software automatically, in real time or on a set schedule, keeping your records current without anyone having to key in a single line.

Reconciliation becomes faster and cleaner because the software is already comparing bank transactions against recorded entries and flagging discrepancies the moment they appear. That way, reporting is not about creating financial reports, but just mouse clicks, and the software pulls accurate data and prepares the reports on demand.

Something else: automation helps you meet homeowners’ expectations for financial transparency. As I said, 73% of homeowners now expect real-time access to their association’s financial data. And on the regulatory side, state-level requirements are increasingly demanding more detailed reporting, stronger reserve maintenance, and tighter compliance standards.

Meeting that expectation requires more than producing accurate reports. It requires making those reports accessible without friction. When a homeowner has to email you or wait until the next board meeting to see a copy of the budget or the latest reserve study, it creates the impression that information is being guarded, even if that’s not the intent at all.

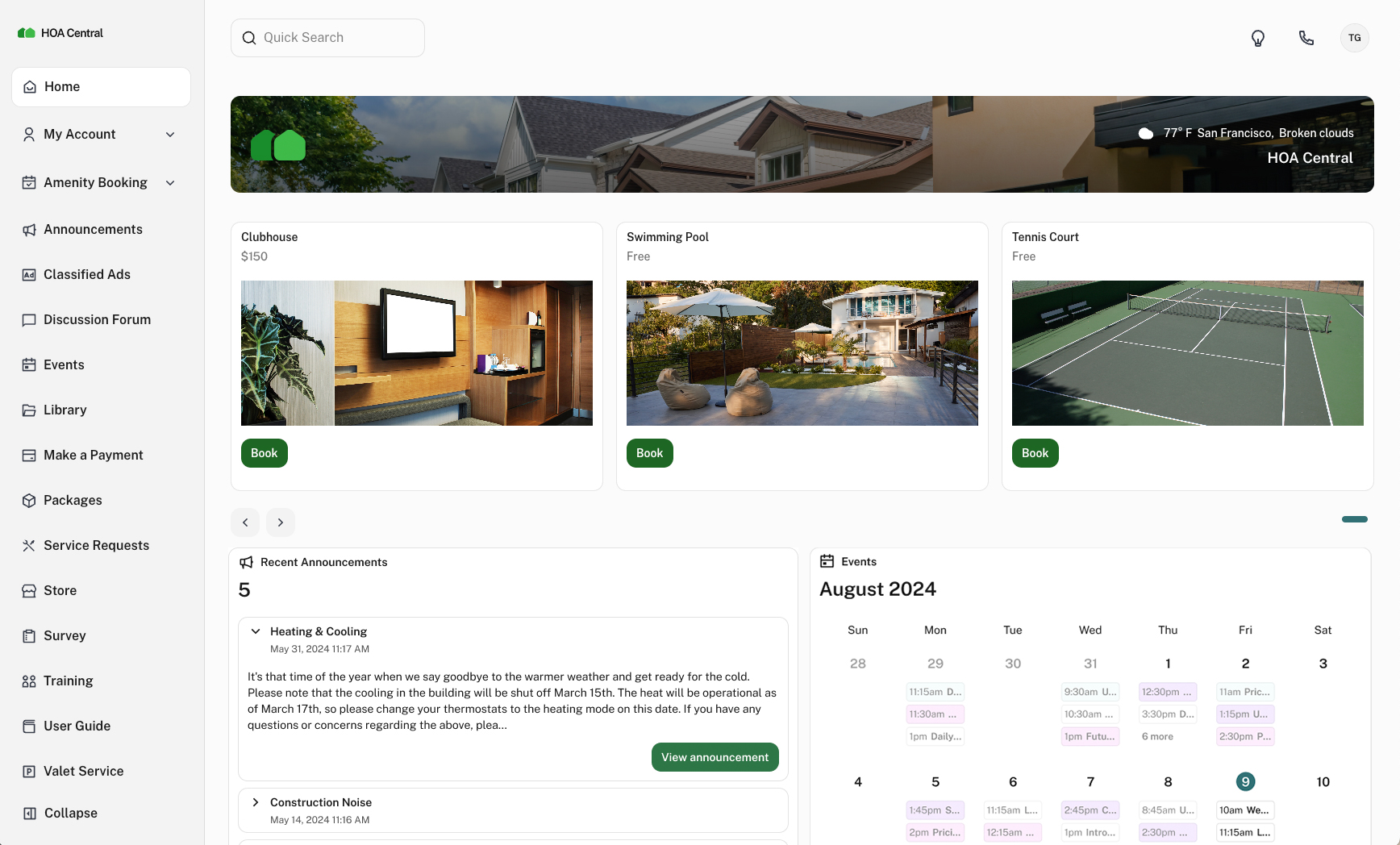

But with automation, homeowners have a platform that puts financial information directly in homeowners’ hands through a self-service portal where they can access documents, review budgets, and check payment history any time they want to. That alone reduces the volume of routine inquiries your team handles and gives homeowners the transparency they expect.

Final thoughts

Everything covered in this blog: the core financial reports, consistent accounting practices, reserve fund discipline, and the right technology platform, has to operate within a legal framework that’s different in every state you work in. As you build out your standardized reporting process, make sure state-specific financial reporting requirements are baked into your workflow from the start. But a smarter solution is to use an end-to-end HOA management platform that already understands the entire process and has the industry accounting standards baked in.