A simple month-end money routine for self-managed boards

Written by: Christine Ponce

Published on: July 7, 2026

Tracking finances is arguably the heaviest part of running a self-managed HOA. There are roughly 373,000 community associations across the United States, home to about 78.1 million residents, and 30 to 40 percent of those associations are self-managed. When you think about what that means in dollar terms, homeowners collectively paid $124.2 billion in assessments in 2025. That means roughly $50 billion a year flows through self-managed boards. That’s not a small number, and the responsibility that comes with it isn’t small either.

Some states have already taken the position that monthly financial oversight isn’t optional. California’s Davis-Stirling Act specifies exactly what a board must review every month: check registers, general ledgers, delinquent receivables, operating and reserve reconciliations, budget-to-actual comparisons, and income and expense statements. Florida takes a more flexible approach, letting associations choose between monthly, bimonthly, or quarterly reviews.

The takeaway isn’t that every state mandates monthly reviews, but it’s a signal that monthly is the right cadence for protecting homeowner money. So, here’s a simple month-end money routine for self-managed boards that will help you protect your community’s finances, support transparency with homeowners, and keep you on the right side of your state’s requirements.

Reconcile the operating and reserve bank accounts

Associations carry at least two accounts: an operating account for day-to-day expenses and a reserve account for long-term capital projects. That separation reflects the two distinct purposes homeowners pay assessments for. Keeping them separate, and reconciling them separately, is what’s called fund balance accounting. It’s the only way to confirm that reserve dollars were used for reserve purposes.

The AICPA’s formal guidance for common interest realty associations, now codified under FASB ASC 972, specifically recommends fund accounting for this reason, recognizing that owners are assessed for two distinct purposes that must remain traceable. The tax implications make the separation non-negotiable: if reserve funds aren’t held separately, the IRS treats them as taxable income to the HOA. And when reserve funds absorb operating shortfalls, the community ends up facing a special assessment for a major repair that the reserves were supposed to cover.

Then state laws also apply. For example, California’s Civil Code §5500 lists operating and reserve reconciliations as two distinct monthly duties, not a combined task done twice. Reconciling the operating account and assuming the reserve is fine because the annual statement looked clean doesn’t satisfy that standard.

On the other hand, Florida law permits operating and reserve funds to share an investment account, but the reserve portion must remain identifiable at all times, and the combined balance can never fall below the reserve floor. So, a blended bank balance won’t tell you whether you’re meeting it. Only a separate reconciliation of the reserve ledger confirms that.

How to reconcile

The reconciliation process is the same for both accounts. Take your ending cash balance, add any deposits in transit, subtract checks that have been issued but haven’t cleared, and confirm the adjusted balance aligns with your accounting records, accounting for interest earned and any bank fees. Any discrepancy between what the bank shows and what your books say should be investigated.

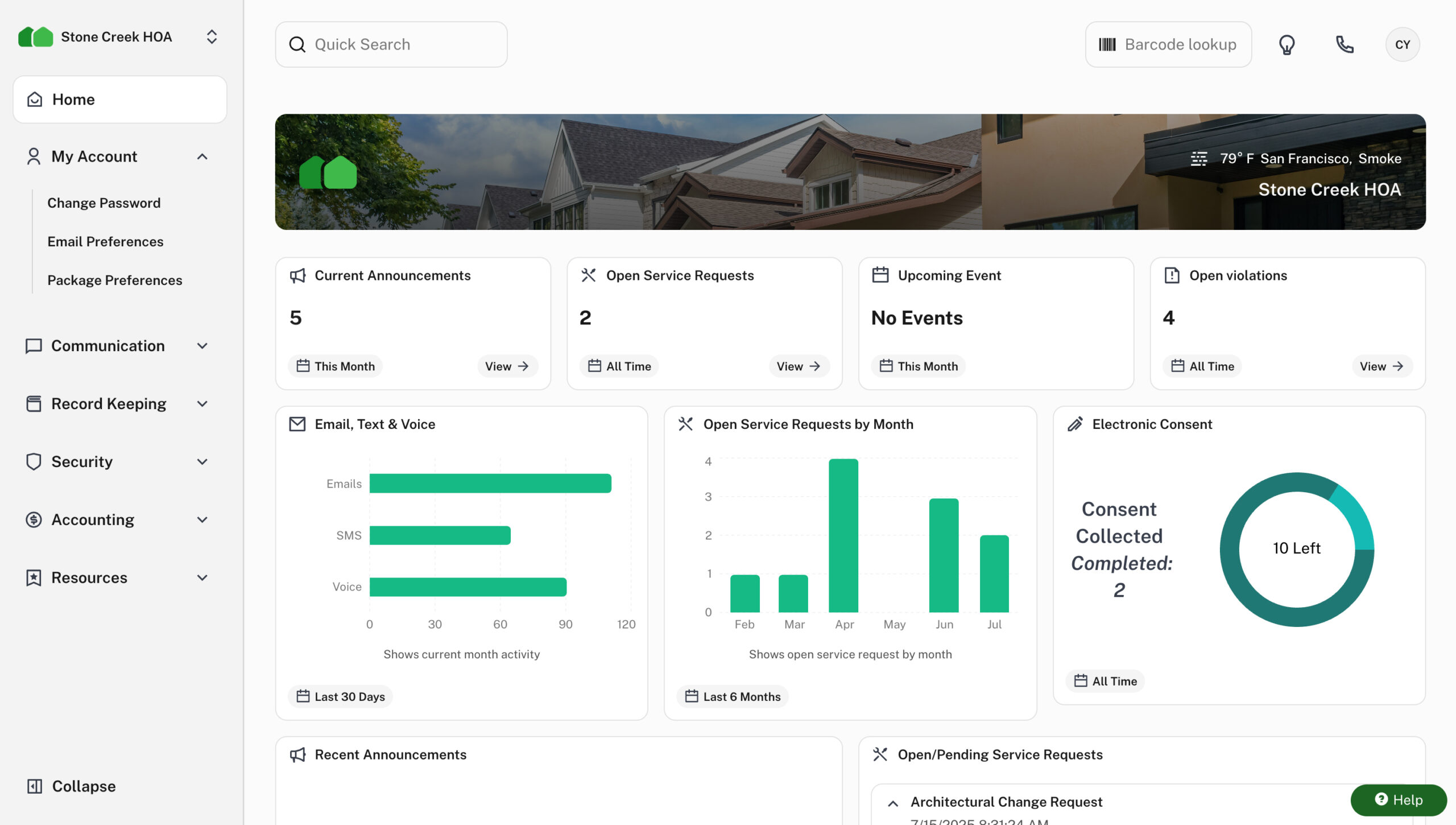

Prepare and share your monthly financial statements

Once the reconciliations are complete, the next step is turning those numbers into something the full board can actually use: a structured packet that gives everyone a documented picture of where the community stands at the close of each month. The format matters here.

FASB ASC 972 establishes that a proper monthly package is a specific set of statements prepared on an accrual basis (or cash basis only when the results wouldn’t differ materially). That means if you improvise your format month to month, you’re drifting away from the standard that lenders, auditors, and future boards will all expect to see.

A complete monthly financial packet covers the balance sheet, income and expense statement, budget variance report, AR aging report, AP report, bank reconciliation, reserve fund summary, and general ledger. Three of those form the core of what every board needs to actively work through at every meeting.

- The balance sheet: It’s a financial snapshot of what the community owns, what it owes, and the state of its fund balances at a specific point in time.

- The income and expense statement: It covers a timeframe such as a month, a quarter, or year-to-date, showing money in and out. Revenue includes assessments, late fees, special assessments, and interest earned. The reason I recommend you review this monthly rather than annually is that problems hide in the details: late-entered invoices and inconsistent coding.

- The budget variance report: It puts actual results next to your approved budget, line by line. If a line item is meaningfully off, the board should be able to explain why.

Financial statements are typically prepared mid-month following the period they cover, once all transactions have been posted. If the financial packet lands at the start of a board meeting, nobody has had a meaningful chance to review it. The standard to aim for: board members receive reports at least five days before the meeting. That’s enough time to read, form questions, and show up prepared to act on what they’ve seen.

Making available the financial statements

On making financials available, most states give homeowners a statutory right to inspect financial records, and the exposure for noncompliance is real. For example, Pennsylvania gives associations 30 days to produce financial statements after a member request, and failing to comply can result in a complaint to the state Bureau of Consumer Protection.

California’s Civil Code §5200 names interim financial statements among the records members can demand, and §5235 allows courts to assess a penalty of up to $500 per written request that’s unreasonably denied, plus the requesting member’s attorney’s fees. That means you can still end up paying real money if multiple homeowners file separate requests.

The lending stakes have sharpened as well. In March 2026, Fannie Mae and Freddie Mac eliminated the streamlined “Limited Review” path for established condo projects. Every purchase and refinance now triggers a full review of the association’s budget, reserve funding, and delinquency status. The board’s ability to produce accurate, current financials quickly has become every owner’s problem. For self-managed boards, the goal isn’t “technically available if someone asks.” It’s about making the statements easy to find on the homeowners’ portal.

Review the aging report and follow up on delinquencies

Pull your accounts receivable aging report at the close of every month. The aging report tells you who owes money and how long that balance has been sitting unpaid. Organized by time buckets, such as Current, 30+ Days, 60+ Days, 90+ Days, it tells you exactly how urgent each situation is and what your next step should be. It’s both a cash flow tool and a collections roadmap.

The reason this report needs monthly attention comes down to what assessments represent. According to the Community Associations Institute, assessment income makes up 85 to 90 percent of the association’s operating budgets. When dues don’t come in, the landscaping invoice and the insurance premium don’t adjust to match. Those bills stay the same, and your operating account takes the hit. Even a small number of delinquent accounts can create a cascading effect on the community’s ability to pay its own obligations.

Recovery data makes the case for monthly ageing report review in the clearest possible terms. According to the Commercial Collection Agencies of America, recovery rates stand at 88.7% when a balance is 30 days past due, and fall to 51.3% at 180 days. ACA International puts first-party recovery at 85% for early-stage delinquencies, dropping to just 11% past 180 days. That means recovery happens early or barely at all. Every month you delay acting on the 60-day column is a month of collectability you won’t recover.

Statutory timelines add urgency from the outside as well. For example, Texas requires a first notice, then a second notice by certified mail at least 30 days later, with no assessment lien permitted before the 90th day after that second mailing, which means a minimum four-month runway before any enforcement action is possible. If you review the aging report only quarterly, you can burn through the statutory notice windows it needs before a lien is even allowed, pushing the entire enforcement timeline back further.

Delinquency followup

Follow up on delinquencies using your documented escalation process. Normally, the standard progression moves from courtesy reminders and late fee notices to formal demand letters, payment plan offers, lien placement, and, as a last resort, legal action. Every delinquent account follows the same timeline, is documented the same way, and has the same opportunities given to each owner.

Review outstanding vendor invoices

Vendor costs represent the largest portion of an association’s operating budget after insurance and reserve contributions. But here’s what the income statement alone won’t tell you: whether the HOA has enough cash right now to meet its near-term obligations. An association can look perfectly healthy on an income statement while running tight on cash when assessment collection is slow, and vendor invoices are stacking up at the same time.

Once you’ve worked through what homeowners owe you, flip to what the association owes others. The accounts payable report shows payee names, amounts due, and due dates. Reviewing it at month-end surfaces which invoices haven’t been paid and why. It also flags completed projects that haven’t been settled and progress payments due on active work.

There’s also an accounting principle worth understanding. Under accrual-basis accounting, a liability exists the moment goods or services are received, even before an invoice arrives. Auditors flag AP as a high-risk area for exactly this reason: a liability that’s been incurred but not yet recorded is invisible unless someone is actively looking for it. In a self-managed community, nobody is doing that in the background. If the unpaid invoice list isn’t reviewed before financials go out, the gap surfaces the following month as a surprise against a budget line that appeared fine.

On the relationship side, contractors who get paid reliably prioritize those clients. Research from Ivalua found that 59 percent of businesses reported losing supplier relationships specifically because of repeated late payments. For a self-managed board that relies on a small roster of trusted vendors, losing one is an operational problem that can take years to rebuild from.

And other than that, when a contractor performs work on common property and doesn’t get paid, that contractor can record a mechanic’s lien directly against the property. Many lenders won’t close on a property with a lien attached, meaning a forgotten invoice can jeopardize refinancing and resale for homeowners.

Simplifying everything with automation

Everything described in this guide, from bank reconciliation and financial statements to aging reports and vendor invoices, can technically be done with spreadsheets and a filing system. But before accepting that as a viable long-term plan, it’s worth being honest about what that actually looks like in practice.

Why manual execution is the weak link

For context, manual reconciliation at a small business with just a handful of accounts takes three to six hours per month, covering only that task. On the AP side, the average manual invoice takes nearly 15 days from receipt to payment, with each one requiring 15 to 30 minutes of active handling once you account for data entry, routing, follow-up, and error correction. That means a complete month-end routine can easily consume an entire weekend of a volunteer treasurer’s month, every month, indefinitely.

The time burden is one problem. Accuracy is another problem. Research on spreadsheet errors shows that experienced users make mistakes in 2 to 5 percent of all formula cells, and those rates compound as spreadsheets grow more complex. For a board reviewing month-end financials built from a hand-assembled spreadsheet, that means the numbers on the table at a board meeting may be wrong.

The second structural vulnerability is what happens when the treasurer leaves. In most self-managed communities, one person carries all the institutional knowledge, from which vendors are on recurring billing and where the files live to how the accounts are organized. When the rotation happens, the incoming treasurer isn’t stepping into a process. They’re trying to reconstruct one.

In fact, research shows that 72 percent of nonprofit leaders say it takes between two and seven days to pull together basic financial data. For a homeowner exercising a statutory inspection right, a board that has to go searching for last month’s numbers has already fallen short of the standard the law sets.

How the right tools turn this into a repeatable routine

The solution isn’t for volunteer boards to become more disciplined at manual processes they were never resourced to run. It’s to automate the parts of the routine that are pure data labor. For instance, with the right software, automated dues collection eliminates manual invoicing and follow-up emails. Bank integrations turn reconciliation from a multi-hour chore into a quick matching exercise because transactions pull in automatically, financial reports generate on demand, and invoice approval workflows route to the right people on time.

Final thoughts

Do those four things every month (reconciling both accounts, preparing and making available financial statements, reviewing delinquencies and reviewing vendor invoices), and you’ll be able to catch and fix problems early. But since these things are time-consuming, prone to human error, and require some degree of accounting knowledge, I highly recommend you automate the routine with an HOA management platform. From there, your work will be to look at the output and make judgment calls.